While the modern computing era in many respects began with the IBM System/360 mainframe and further expanded with the minicomputer, normal consumers didn’t start encountering computers until the personal computer. And, while mainframes are technically still around (while minicomputers are decidedly not), what is unique about the PC is that it is very much still a part of modern life.

In fact, one of the defining characteristics of the three major epochs of consumer computing – PC, Internet, and mobile – is that they have been largely complementary: we didn’t so much replace one form of computing for another insomuch as we added forms on top of each other.1 That is why, as I argued in Peak Google, many of the major tech companies of the last thirty years haven’t so much been disrupted as they have been eclipsed by new companies built during new epochs. All of the attention and relevance in tech especially is focused on emerging and growing companies, even as mature giants reap massive profits.

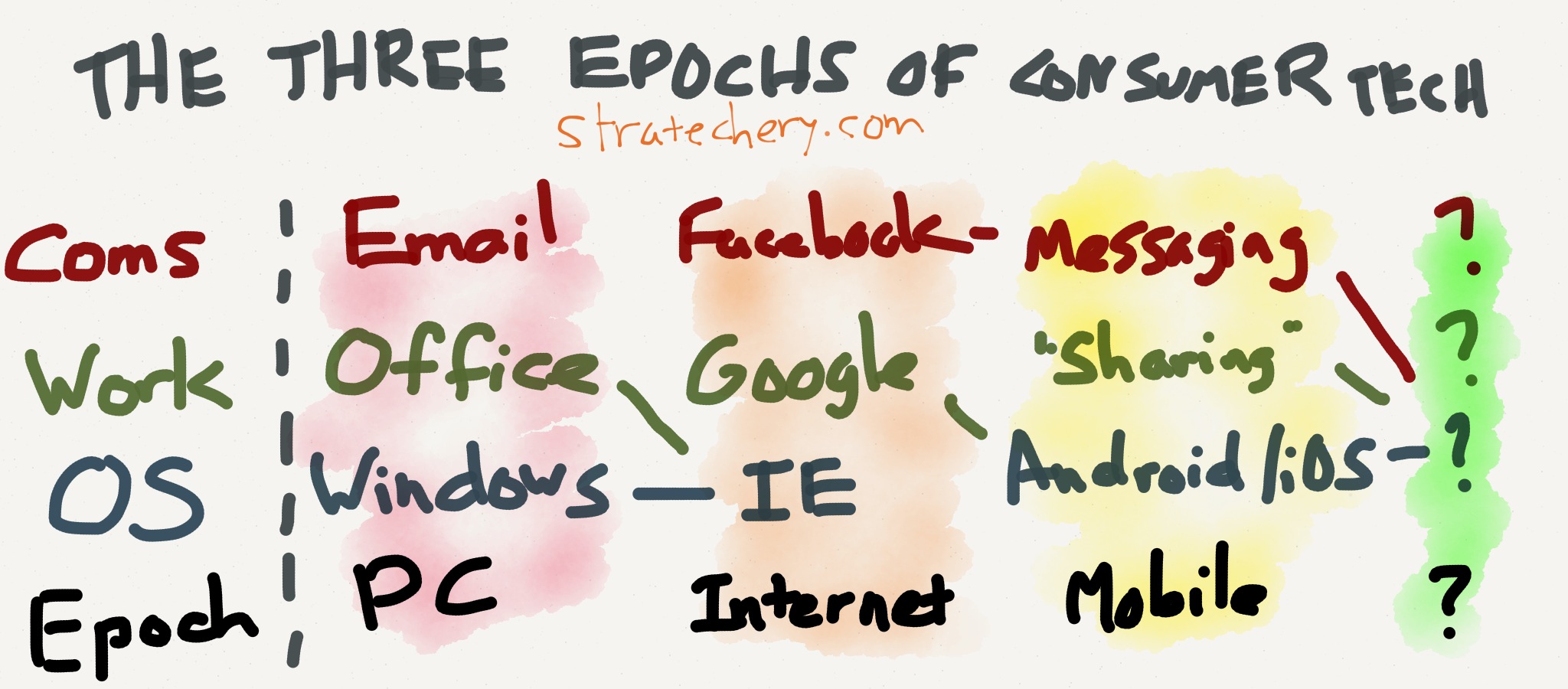

Every epoch has had four distinct arenas of competition that emerge in order:

- The core technology

- The operating system (i.e. the means by which the core technology is harnessed)

- The killer use case for:

- Work/Productivity

- Communication

Certainly computers can be used for more than work/productivity or communication, but those two use cases are universal and lead to the biggest winners and most important companies.

Epoch One: The PC

The PC epoch began on August 12, 1981. That is the day the IBM Personal Computer was released with an Intel 8088 processor running Microsoft DOS 1.0. This open design was the core technology; the only proprietary IBM chip inside was the BIOS, which was soon reverse-engineered by Compaq who released the first “PC compatible” computer 17 months later.

The operating system for the PC has been owned by Microsoft from the beginning; the Mac has garnered a profitable share at times (including today), but Windows versus Mac wasn’t really a contest, because with DOS Microsoft had already won the game.

The killer application for work/productivity on the PC was the spreadsheet specifically, and front-office general-purpose apps broadly, including the word processor and presentation software. While it took much longer, Microsoft eventually came to dominate this space as well with the Office suite.

The killer communication application on the PC ended up being open as well: email. Still, even here the most dominant player, at least in the corporate space (which is what mattered), was Microsoft once again, with Exchange on Windows Server. For all you young folks that can’t understand why us old people looked at Microsoft for so long with a mix of reverence and fear, well, now you know: the company in the end owned nearly every component of the PC epoch, and for all their struggles to remain relevant, Microsoft has never struggled to be profitable.

Epoch Two: The Internet

The Internet epoch began 14 years after the PC epoch, nearly to the day, with the Netscape IPO on August 9, 1995. The core pieces of the Internet had been around for years, and the World Wide Web was developed by Tim Berners-Lee and formally announced in August 1991 (clearly August is an auspicious month), but it was the “Netscape Moment” that woke everyone up to the possibilities of the Internet.

Here the battle for the OS – also known as the browser – was much more fraught. Netscape jumped out to a huge lead, holding over 90 percent usage share, but Microsoft fought back by bundling Internet Explorer for free with Windows, and, truthfully, from Internet Explorer 3 on, by having a better product. Eventually it was Internet Explorer that had over 90 percent market share, and Microsoft felt they had won the Internet.

However, it ultimately turned out that the browser wasn’t what mattered. Instead, the Internet made information, which for so long had been a scarce resource, abundant. So abundant, in fact, that it seemed impossible to make sense of it all, at least until Google came along. Search was the killer work/productivity application on the Internet: now you could instantly find the answer to just about anything on Google, and the company rightly dominated the category.

The killer communications app took even longer to appear, but it solved a problem not dissimilar to Google: Facebook didn’t just let you communicate with people you knew, it came to understand how nearly every single person online was connected. And, as the number of people online continued to grow, so did Facebook. For all the misguided talk of Facebook being under threat, the reality is that its position as the default interconnect between every person on earth is as secure as ever.

Epoch Three: Mobile

I would like to choose Google’s acquisition of Android as the beginning of the mobile epoch, just because it happened in August (2005, in this case), but the date that matters is January 9, 2007, when Steve Jobs announced Apple’s iPhone. The core technology was the smartphone; while Nokia, Palm and Blackberry had been building precursors, it was the iPhone with its multitouch screen, unfettered Internet access, and (eventual) App Store that defined the category.

Unlike the previous two eras, there has not been a single winner when it comes to the OS. In contrast to the PC, Apple was first-to-market. More importantly, smartphone buyers and smartphone users are usually always the same person, which allows Apple to differentiate itself according to the user experience and thus retain the top slice of the market. Android, meanwhile, was not only the first credible alternative to iOS, but also free, making it the operating system of choice for desperate phone OEM’s everywhere, and over time, allowing the OS to gobble up the vast expanses of the market driven primarily by price.

Right now the operating system war is roughly at equilibrium; with the iPhone 6 it seems likely that Apple is stealing some share back from Android, particularly at the high end, but Android is simultaneously pushing down and out into the developing world, expanding both its share of the market and the market as a whole. What is more interesting is looking at who will emerge in the communications and work/productivity space.

The Mobile Work/Productivity Space

If the PC epoch was about being omnipotent – computers can do everything, better! – and the Internet epoch about being omniscient – with Google, you can know everything – mobile is about being omnipresent. By virtue of being, well, mobile, smartphones extend computing to every aspect of our daily lives. That is why the killer applications and dominant companies in the mobile work/productivity space will be defined by how they bridge the online and offline worlds.

Chief among these companies, at least in my opinion, is Uber: the long-term potential of the company is about being the physical network that connects everything. Their success, though, is by no means assured. Moreover, there are other interconnects, like Airbnb or Postmates or Instacart, which are targeting verticals instead of everything everywhere. These examples are all built on the “sharing” economy, the sheer logistics of which are only possible because of smartphones.

Other work/productivity applications may continue to emerge – cameras are very interesting here – but I suspect the dominant companies have already been started.

The Mobile Communications Space

I’ve already made my case for the winning communications application back in February (the day before Facebook acquired WhatsApp) in an article called Messaging: Mobile’s Killer App:

Still, it’s only recently that the killer app for this era, when the nodes of communication are smartphones, has become apparent, and it is messaging. While the home telephone enabled real-time communication, and the web passive communication, messaging enables constant communication. Conversations are never ending, and friends come and go at a pace dictated not by physicality, but rather by attention. And, given that we are all humans and crave human interaction and affection, we are more than happy to give massive amounts of attention to messaging, to those who matter most to us, and who are always there in our pockets and purses.

As I note in that article, messaging is compelling not just because it enables a new kind of communication, but also because it is a platform in and of itself. Already LINE and WeChat are leveraging that platform to push applications, particularly games, and making money on the back end. In the future, I expect both to be major channels for direct marketing between companies and consumers, and in fact WeChat has pushed even further in China, offering e-commerce, taxi services, and more all through their messaging app.

It seems likely that the messaging battle will result in multiple winners: LINE already owns Japan, Taiwan, and Thailand, and is competitive in Indonesia and (they claim) in Spain, while WeChat is dominant in China. WhatsApp has the largest share worldwide, but that product is the furthest from being a real platform and a real business.2 Messenger is clearly seeking to mimic LINE and WeChat, and is the likely winner in most Western countries.3

What’s Next

While the introduction of the iPhone seems like it was just yesterday (at least it does to me!), we are quickly approaching seven years – about the midway point of this epoch, if the PC and Internet are any indication.4 I sense, though, that we may be moving a bit more quickly: the work/productivity and communications applications have really come into focus this year, and while the battle to see what companies ride those applications to dominance will be interesting, it’s highly likely that the foundation is being laid for the core technology of the next epoch:

- Wearables is a possibility, and it certainly seems that Apple is trying to accelerate the category with their ambitious Apple Watch rollout. However, no matter how good the Apple Watch is, I’m not sure it’s an epoch definer, especially if it cannot truly stand alone

-

Bitcoin is a definite possibility, particularly if there ends up being a “tick-tock” to epochs: device (PC), then protocol (Internet), device (smartphone), then protocol (Bitcoin). Blockstream, an attempt to create sidechains for non-monetary applications that run on top of Bitcoin, is particularly interesting in this regard5

-

Both of the mobile applications that I identified could be core technology for the next epoch: were Uber to become ubiquitous, could businesses be built on top of it? What would such an operating system look like? An out-there idea to be sure, but in the realm of possibility.

More likely is that the messaging services become so dominant that they render the underlying mobile platform unimportant. This too would be similar to the effect of the Internet on the PC: the biggest reason the Mac was able to make a comeback from near death was because the Internet – and web apps – ran everywhere. It didn’t matter what browser6 or OS was on your actual PC. Similarly, if all essential apps and servers are routed through your messaging service, then the underlying OS – whether iOS or Android – is increasingly irrelevant. In fact, I strongly believe this is the future in China in particular, one more reason why Apple is investing so strongly in non-tangible qualities like fashion.

What seems clearer is that today’s giants will continue owning their various categories in the context of their various epochs, even as they fade to – or continue in – irrelevance.

- Microsoft still sells a lot of Windows licenses, and businesses especially still rely on Office. Still, it’s striking how unimportant Microsoft’s defensive move into browsers ended up being, especially when you think about…

-

Google seems strong, but as I’ve written previously, there is a lot about the company that feels like Microsoft: just as Microsoft jumped into the next epoch at the OS level for defensive reasons, Google too jumped ahead, also at the OS level, and also for defensive reasons. “Free” figured prominently in both strategies, and in the long run, it’s worth considering the possibility that Google’s Android dominance will have as much long term value to the company as Microsoft’s dominance of browsers – i.e., not very much at all. Ultimately, I expect an increasing amount of Google’s energy to go towards taking away what Microsoft has left: Chromebooks versus Windows, and Google Apps versus Office

-

Facebook is in a unique position: while they were started as an Internet company, they were an exceptionally young one, and have clearly made a successful jump to mobile. Their position in mobile, though, while secure, is by no means dominant, and it’s interesting that they are in fact following the Microsoft/Google playbook: both the WhatsApp and Oculus acquisitions were about securing a stake in the OS for the next epoch

-

Apple, as always, is following the beat of their own vertically-aligned drummer. They have (usually) good-enough services that work only on their exceptional hardware, and an OS advantage that matters to some number of people. More important in mobile is their ecosystem advantage: Apple has the best customers, devices, and OS, and thus gets the best apps, even though Apple isn’t exactly a benevolent ecosystem manager (members-only). I expect the company’s mobile position to be secure – they’re not going anywhere – and if wearables is the next epoch they are the best positioned: personal is what Apple is best at, and that’s exactly what wearables are

-

Amazon’s most important role in these epochs is AWS, where they are locked in increasingly fierce competition with Microsoft and to a lesser extent Google for cloud dominance. It’s worth noting that Amazon is attacking this space from a very different direction: AWS is another low-margin product in a company built on low-margins, while Microsoft and Google have tons of cash from their high margin core but little experience competing on price

Do note, there are a lot of fascinating products and companies – Pinterest, Twitter, Instagram, even Xbox – that I have not covered: it’s not that they aren’t important, but they aren’t epochal (there’s a decent chance this is where Apple Watch ends up). And, of course, there is the whole enterprise world, itself undergoing real disruption (members-only) from software as a service and the explosion of mobile. What an industry!

I have previously written Strengths-Weaknesses-Opportunities-Threats analyses for these five companies for Daily Update subscribers.

If you would like to read these analyses and receive similar notes every day in your inbox, why not treat yourself to an early Christmas present and sign up for Stratechery Daily Updates?

And have a very Merry Christmas!

There is much confusion about this, largely because mobile is taking an ever greater percentage of time. However, most of that is additive. PC usage has in fact remained mostly static ↩

Thanks to Facebook, of course, Jan Koum and company don’t need to worry about actually making money and can continue taunting competitors. Needless to say, I’m less impressed than Koum ↩

iMessage is a good product and a great differentiator, but the fact it’s (rightly) not cross-platform means it’s not a player here ↩

By the way, it’s worth noting that the midpoint of the previous two epochs – 1987 and 2000 – saw major crashes. Cross your fingers ↩

I am still very concerned (members-only) about 51% attacks, and yes, I know all of the (ultimately trust-based) arguments against it ↩

Mostly ↩