I am usually quite conservative when it comes to how much time, data, and effort I am willing to put into a product from a new startup: too many go out of business or are acquired-and-sunset, and who wants to go to the effort twice?

Dropbox, though, was something else entirely: the initial release in 2008 was so good, and filled such a need, that I switched all of my most important data there immediately and I’ve never left, even though I have lots of free data storage included with other SaaS software plans. Indeed, I was so convinced that Dropbox wasn’t going anywhere that I felt no compunction about using Dropbox (plus a bit of Apple Script) as a de facto syncing system for a school I was working at; it has been ten years, the school has expanded to multiple locations, and every classroom still has the exact same set of files thanks to a product that does exactly what it promises. And now the company behind it is going public — I knew it!

Still, even if the utility and durability of Dropbox’s product was immediately apparent, the long-run trajectory of its business is, even with the release of the company’s S-1, less so.

Dropbox Versus Box and the Question of Lifetime Value

Dropbox and Box have always been compared, and for a rather obvious reason: the core offering of both companies is cloud storage. Said comparison, though, mostly serves to highlight that while the two companies might have similar products, there are so many other ways to be different.

First and foremost, Box has, since the earliest days of the company, been focused on enterprise customers, while Dropbox started out as a consumer product. I explained why this mattered in 2014’s Battle of the Box:

Dropbox’s model makes sense theoretically, but it ignores the messy reality of actually making money. After all, notably absent from my piece on Business Models for 2014 was consumer software-as-a-service. I’m increasingly convinced that, outside of in-app game purchases, consumers are unwilling to spend money on intangible software. That is likely why Dropbox has spent much of the last year pivoting away from consumers to the enterprise.

There are multiple reasons why the latter is a more attractive target for all software-as-a-service companies, especially those focused on data:

- Consumers need to be convinced of the value of their data…

- Consumers have multiple free options…

- Consumers are hard to market to…

- For consumers, collaboration is an edge case…

- Building a platform for consumers is incredibly difficult…

I concluded by arguing that $10 million invested in Box at its-then $2 billion valuation was a better bet than the same $10 million invested in Dropbox at its-then $10 billion valuation; given that Box has a $3.2 billion market capitalization while Dropbox is hoping its IPO will clear that same $10 billion mark, I’m (fake) rich!

Dropbox, though, has indeed pivoted: the company said in its S-1:

Of our 11 million paying users, approximately 30% use Dropbox for work on a Dropbox Business team plan, and we estimate that an additional 50% use Dropbox for work on an individual plan, collectively totaling approximately 80% of paying users.

Still, significant differences remain: Dropbox’s customer base, thanks to all those consumers, is over 500 million users (Dropbox announced 500 million signups last March, but explained in its S-1 that it had culled what were apparently ~100 million inactive accounts over the last year), while Box, as of last quarter, had only 57 million registered accounts. On the other hand, 17% of Box’s users had paid accounts; only 2% of Dropbox’s did. This contrast in efficiency gets at the biggest difference between the two companies: to whom they sell, and how they go about doing so.

Box sells to big companies using a traditional sales force; free accounts exist primarily to enable temporary collaboration with paid accounts, as well as trials. There is a self-

serve option, but that’s not the point: Box notes in its financial filings that “Our marketing strategy also depends in part on persuading users who use the free version of our service to convince decision-makers to purchase and deploy our service within their organization”. In other words, when it comes to Box’s ideal customer, the CIO decides for everyone all at once.

For Dropbox, on the other hand, self-serve is the most important channel by far. The company brags that “We generate over 90% of our revenue from self-serve channels — users who purchase a subscription through our app or website.” Dropbox has a sales team, but as it notes in its S-1, the team “focuses on converting and consolidating these separate pockets of usage into a centralized deployment. Nearly all of our largest outbound deals originated as smaller self-serve deployments.”

There are pros and cons to both approaches. Start with the obvious difference: customer acquisition cost. While the two companies spent a comparable amount on sales and marketing in the third quarter of 2017 ($81.7 million for Box, and $74.7 million for Dropbox1), for Box that represented 63% of revenue; for Dropbox it was only 26%.2

However, the two numbers aren’t as comparable as they seem: specifically, Box’s Sales and Marketing includes the infrastructure and support costs of those free users; Dropbox’s doesn’t. Rather, the company includes those costs in its Cost of Revenue, which is a big reasons Dropbox’s gross margin of 68% trails Box’s 73%.3 And, by extension, we don’t really know what Dropbox’s customer acquisition cost is.

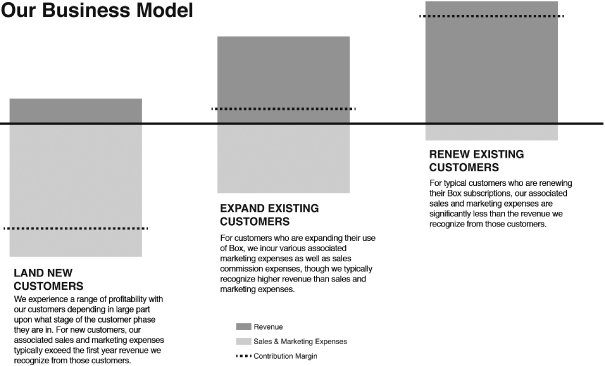

There is another advantage of selling to top-down decision-makers: the opportunity to build solutions for specific needs, and charge accordingly. This has enabled Box to achieve negative churn: in all of its cohorts the company is increasing its revenue-per-user by a faster rate than it is losing users overall, which means revenue-per-cohort increases over time. The company explained this in its amended S-1:

Our business model focuses on maximizing the lifetime value of a customer relationship. We make significant investments in acquiring new customers and believe that we will be able to achieve a positive return on these investments by retaining customers and expanding the size of our deployments within our customer base over time…

We experience a range of profitability with our customers depending in large part upon what stage of the customer phase they are in. We generally incur higher sales and marketing expenses for new customers and existing customers who are still in an expanding stage…For typical customers who are renewing their Box subscriptions, our associated sales and marketing expenses are significantly less than the revenue we recognize from those customers.

Box went on to give numbers for specific cohorts; Dropbox, unfortunately, was significantly less specific:

As we continue to innovate and optimize our go-to-market strategy, we have successfully increased monetization for subsequent cohorts. Comparing January cohorts from the last three years, at virtually every point in time after signup, the January 2017 cohort generated a higher monthly subscription amount than the January 2016 cohort, which in turn generated a higher monthly subscription amount than the January 2015 cohort.

This sounds good, until you actually try to figure out what it means. Is the January 2017 cohort monetizing more because users are paying more quickly, or because there are more users? How many of those users are churning, and is there an increase in revenue-per-customer to counteract that?

Dropbox’s S-1 doesn’t give the answer to the first two questions, but the answer to the third seems to be “no”. Average revenue per paying user is actually down from 2015 ($113.54 to $111.91), although slightly up from 2016 ($110.54). Given the model, though, this isn’t a surprise: the only way to serve a massive user-base efficiently is to have a fairly standardized offering; creating and selling differentiating features that increase the average revenue per paying customer doesn’t scale.

There is one other big advantage in terms of Dropbox’s model, at least from a founder and early investor perspective: the tradeoff of Box earning ever-increasing amounts of revenue per paying customer is the amount it takes to land that customer in the first place. This is why Box’s losses were so large, and why founder and CEO Aaron Levie was so diluted by the time the company finally IPO’d (Levie owned just over 5% of Box at the time of IPO). Dropbox founder and CEO Drew Houston, on the other hand, still owns 25%, and early investor Sequoia Capital another 23%; a founder retaining that much ownership is much more characteristic of a consumer company than an enterprise one — which is exactly how Dropbox started.

Dropbox Versus Atlassian and the Question of Market Size

Still, Houston’s ownership stake pales in comparison to Scott Farquhar and Mike Cannon-Brookes, co-founders and co-CEOs of Atlassian, who owned 37.7% of the company each when it IPO’d two years ago. Not coincidentally, Atlassian was very much a pioneer in the self-serve model when it comes to enterprise software, and as I wrote at the time of their S-1, it helped that the company was selling to developers:

Agile was largely developer-driven, another factor that worked in JIRA and Atlassian’s favor. Developers are, quite obviously, much more willing to do their own research on products, download and trial software from the Internet, and if they like it, proselytize to other developers even if they don’t work for the same company. In other words, of all the different types of enterprise software, development tools are uniquely suited to spreading somewhat virally without the need for a traditional sales force.

One of the big questions at the time of Atlassian’s IPO was just how big their market was — specifically, could the company start selling beyond its developer base? So far the results are encouraging: JIRA Service Desk, the company’s attempt to expand its JIRA project management software to non-developer teams, is in over 25,000 organizations, and the company overall continues to grow both by adding new customers and by selling more products to existing customers.

This is the second question for Dropbox, beyond the uncertainty around its customer acquisition costs and churn: to what extent can it expand its market? On the positive side, those 500 million users are all potential customers; on the other, the vast majority of them have avoided paying for ten years — the proportion of paid users has barely budged over time. And again, Dropbox hasn’t developed ways for its already paying customers to pay it more.

The potential is certainly there: note that Atlassian’s growth, with a similar model to Dropbox’s, is far out-pacing Box’s — 42% in 3Q 2017 (Atlassian’s FY Q1 2018), compared to 26% — but then again it is far out-pacing Dropbox’s 30% as well. That Dropbox’s revenue growth is slowing suggests the company is ultimately a niche player.

Dropbox Versus Slack and the Question of the Enterprise OS

I once thought that Dropbox — and Box, for that matter — could be more than that; in 2014 I wrote Box, Microsoft, and the Next Enterprise Platform:

Pure storage isn’t a great business. The cost is trending towards zero, as noted by Levie himself. Data, though, is priceless; it can’t be replaced, and it’s the essence of what makes a particular organization unique…Just because the operating system is no longer the platform does not mean that the need – and opportunity – for a platform does not exist. Something needs to tie together all those computing devices, and data, which needs to be everywhere, is the logical place to start.

Dropbox made a similar argument in its S-1:

Our modern economy runs on knowledge. Today, knowledge lives in the cloud as digital content, and Dropbox is a global collaboration platform where more and more of this content is created, accessed, and shared with the world. We serve more than 500 million registered users across 180 countries…

Our market opportunity has grown as we’ve expanded from keeping files in sync to keeping teams in sync. Today, Dropbox is well positioned to reimagine the way work gets done. We’re focused on reducing the inordinate amount of time and energy the world wastes on “work about work” — tedious tasks like searching for content, switching between applications, and managing workflows.

The shift in focus from data to people is one I made myself in 2015; commenting on that Box OS article above, I wrote:

I think, in retrospect, I outsmarted myself: companies aren’t made of data, they’re made of people, just like every other single institution on earth. And, as I noted in the context of Facebook, what people love to do, more than anything else in the world, is communicate. Why wouldn’t you start there?

To that end Dropbox is marketing itself to investors as a collaboration company, and heavily emphasizing Dropbox Paper. In the meantime, though, another company — the one I was writing about in that excerpt — has entered the scene: Slack.

It’s hard to see anyone — including Microsoft — having a bigger opportunity than Slack.4 The trend in every aspect of computing is higher and higher levels of abstraction, and that doesn’t apply just to things like programming languages. In the case of platforms, the operating system of the PC used to really matter, and then the Internet came along and it didn’t. Similarly, in mobile, the operating system, whether that be iOS or Android, used to really matter, but now it doesn’t. In the consumer space, Facebook or WeChat runs on both, and that is far more important to the day-to-day experience of the vast majority of people.

It turns out that “mobile” is not about devices, but rather, at a fundamental level, about computing anywhere; to differentiate between PCs or phones is an ultimately meaningless exercise. They are simply different form factors of effectively identical devices, the purpose of which is to connect us to the cloud (consumer or enterprise). And, by extension, if the device is simply an implementation detail, then the operating system that runs on that device is a detail of a detail.

What matters — what always matters! — is what actual users want to do, and what jobs they want to accomplish. And, whatever they want to do almost certainly involves communicating, which means Slack and its competitors are the best-placed to be the foundational platform of the cloud epoch. More broadly, humans are social creatures: why should we be surprised that social networks are primed to be the most important businesses of all?

It’s been two years since I wrote that, and while Slack is still growing, albeit more slowly, the question of which company controls the future of enterprise computing remains an open one. Is it Amazon via infrastructure, Microsoft via infrastructure and identity and email, Slack via chat? Google via all-of-the-above?

What seems clear is that it won’t be Dropbox — both because files weren’t the right route and also because the company spent far too much time and energy chasing a non-existent consumer opportunity — but that’s ok. There is still value — at least $10 billion in value, I’d bet — in doing a job and doing it well, whether that be as a startup in 2008 or a public company in 2018. We still need to share files (and yes, collaborate on them), and will need to do so for a very long time, and Dropbox does it better than anyone. I just wish Dropbox’s S-1 didn’t make it so difficult to figure out just how much value there might be.

I wrote a follow-up to this article in this Daily Update.

This number jumped to $102.9 million in the fourth quarter, which is a much larger jump than any previous fourth quarter, perhaps in anticipation of the IPO filing ↩

Per the previous footnote, in the fourth quarter sales and marketing was 34% of revenue ↩

More on Dropbox’s dropping Cost of Revenue tomorrow ↩

Note that I said “opportunity”; opportunity means it’s possible, not that it’s necessarily going to happen ↩