As a reminder, each week, every Friday, we’re sending out this overview of content in the Stratechery bundle; highlighted links are free for everyone. Additionally, you have complete control over what we send to you. If you don’t want to receive This Week in Stratechery emails (there is no podcast), please uncheck the box in your delivery settings.

On that note, here were a few of our favorites this week.

The Cost of AI. The key to understanding and analyzing tech has been appreciating the implications of zero marginal costs, which govern the economics of everything from chips to software to services. AI services generally fall under the same rubric — fixed costs in terms of data centers and chips matter more than marginal costs (mostly electricity) — but the worsening shortage in compute means it is opportunity costs that matter more than ever. Companies will have to make hard choices, and the biggest loser might be the serially unfocused OpenAI. — Ben Thompson

What Is Amazon Doing with Globalstar? Earlier this week Amazon announced an $11.8 billion deal to purchase Globalstar satellites in what was billed as a move to ramp the company’s competition with Elon Musk and Starlink There may be more going on with that deal, though, and Wednesday’s Daily Update explored what Apple’s role might have been. We went deeper on all this on Friday’s episode of Sharp Tech, and I loved the segment as a window into Amazon’s motivations for satellite investments generally, and the questions surrounding this deal specifically. —Andrew Sharp

Nico Rosberg on Racing and Investing. As a religious F1 fan I’m obligated to recommend this week’s Stratechery Interview with Nico Rosberg, a terrific conversation with a former world champion in Formula 1 and a recent entrant into the world of venture capital. Come for stories of surviving the mental grind of F1 and why Rosberg walked away at the pinnacle of his career, and stay for a study of someone who looks for an edge in everything he does, understands his advantages, and has been very strategic about leveraging them to succeed in a completely different world. You wouldn’t think a famous F1 driver has lessons that could be applicable to anyone, but I was pleasantly surprised. —AS

What the NBA Needs Right Now Is Anyone But OKC — After a long and mediocre regular season, the NBA Playoffs bring new hope for the league and fans alike. We just need one team to lose.

Dithering with Ben Thompson and Daring Fireball’s John Gruber

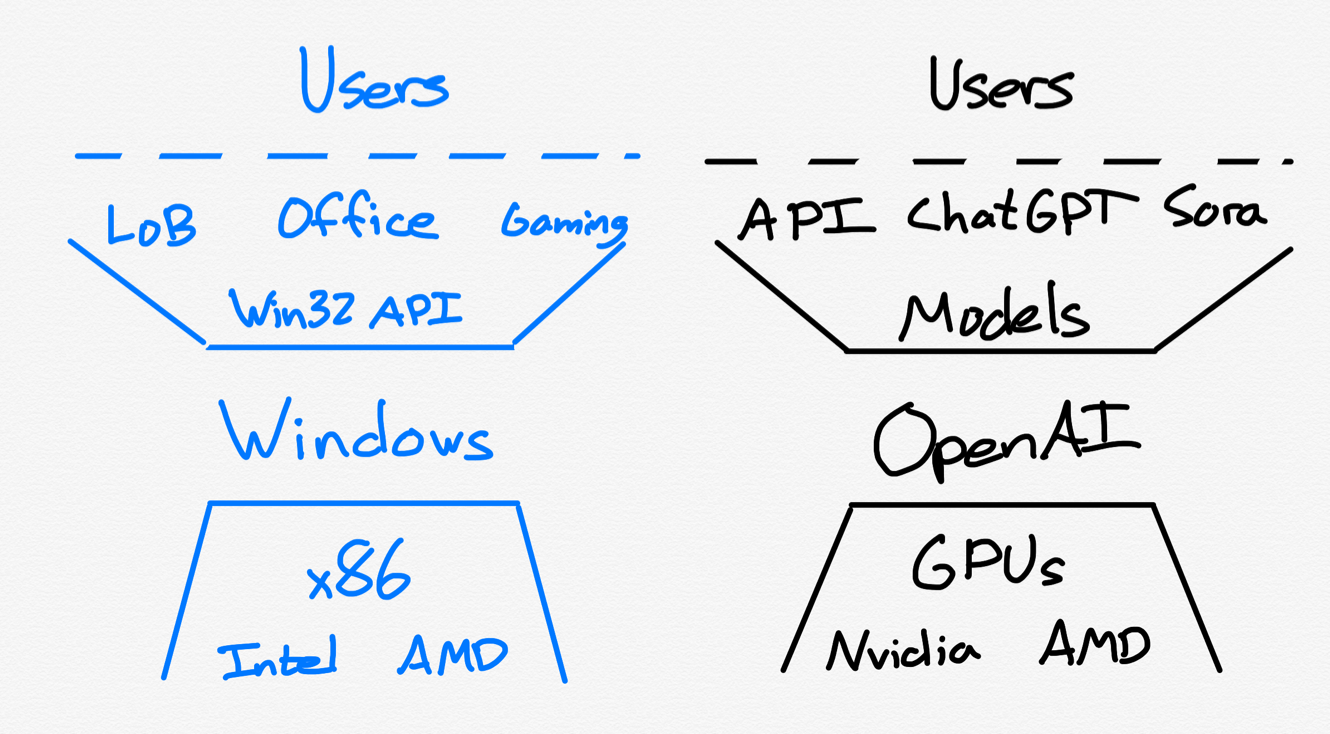

In January 2025, Doug O’Laughlin at Fabricated Knowledge declared that o1 and reasoning models marked the end of Aggregation Theory:

I believe that there is no practical limit to the improvements of models other than economics, and I think that will be the real constraint in the future. It is reasonable that if we spent infinite dollars on a model, it would be improved. The problem is whether infinite dollars would make sense for a business.

That is going to be the key question for 2025. How do the economics of AI make this work? One of the core assumptions about the internet has just been broken. Marginal costs now exist again, meaning that most hyperscalers will become increasingly capital-intensive.

The era of Aggregation Theory is behind us, and AI is again making technology expensive. This relation of increased cost from increased consumption is anti-internet era thinking. And this will be the big problem that will be reckoned with this year. Hyperscaler’s business models are mainly underpinned by the marginal cost being zero. So, as long as you set up the infrastructure and fill an internet-scale product with users, you can make money.

This era will soon be over, and the future will be much weirder and more compute-intensive. Looking back on the 2010s, we will probably consider them a naive time in the long arc of technology. One of our fundamental assumptions about this period is unraveling. This will be the single most significant change in the technology landscape going forward.

Aggregation Theory was, if I may say so myself, the single best way to understand the 2010s, particularly consumer tech. It explained the dynamics undergirding Google and Facebook’s dominance, as well as the App Store and Amazon’s e-commerce business; it was also a useful (albeit incomplete) framework to understand an entire host of consumer services like Uber, Airbnb, and Netflix.

It’s worth pointing out, however, that some of the critical insights undergirding Aggregation Theory are much older, and are embedded in the fundamental nature of tech itself. They are, as O’Laughlin notes, rooted in the concept of zero marginal costs.

Marginal Costs

Marginal costs are how much it costs to make one more unit of a good. Consider a widget-making factory:

You need land for the factory

You need machines for the factory

You need electricity to operate the machines

You need humans to operate the machines

You need the raw material for the widgets

Land and machines are clearly fixed costs; you have to have both to get started, and you are paying for both whether or not you make one more widget. Raw material, on the other hand, is clearly a marginal cost: if you make one more widget, you need one more widget’s worth of raw material. When it comes to physical goods, electricity and humans are also marginal costs: you need more or fewer of them depending on whether you make more or fewer widgets.

Where marginal costs matter is that they provide a price floor. Companies will operate unprofitably because profit and loss is an accounting concept that incorporates depreciation, i.e. your fixed costs. For example, imagine that a company spent $1,000 on a factory to make widgets that have a marginal cost of $10: as long as the price of widgets is >$10 the company will make them even if they don’t earn enough money to cover their depreciation costs (i.e. they operate at a loss) because at least they are still making a marginal profit on each widget (what the company may not do is invest in any more fixed costs, and, eventually, will probably go bankrupt from interest on the debt that likely financed those fixed costs).

I explain all of this precisely because it’s almost completely immaterial to tech. First, there generally are no raw material costs, because the outputs are digital. Second, because there are no raw material costs, and because the fixed costs are so large, electricity and humans are generally treated as fixed costs, not marginal costs: of course you will run your servers all of the time and at full capacity, because every scrap of additional revenue you can generate is worth it.

AI very much fits in this paradigm: the output is digital, and while AI chips use a lot of electricity, the cost is a fraction of the cost of the chips themselves, which is to say that no one with AI chips is making marginal cost calculations in terms of utilizing them. They’re going to be used! Rather, the decision that matters is what they will be used for.

Opportunity Costs

Consider Microsoft: last quarter the company missed the Street’s Azure growth expectations not because there wasn’t demand, but because the company decided to use its capacity for its own products. CFO Amy Hood said on the company’s earnings call:

I think it’s probably better to think about the Azure guidance that we give as an allocated capacity guide about what we can deliver in Azure revenue. Because as we spend the capital and put GPUs specifically, it applies to CPUs, the GPUs more specifically, we’re really making long-term decisions. And the first thing we’re doing is solving for the increased usage in sales and the accelerating pace of M365 Copilot as well as GitHub Copilot, our first-party apps. Then we make sure we’re investing in the long-term nature of R&D and product innovation. And much of the acceleration that I think you’ve seen from us and products over the past a bit is coming because we are allocating GPUs and capacity to many of the talented AI people we’ve been hiring over the past years.

Then, when you end up, is that, you end up with the remainder going towards serving the Azure capacity that continues to grow in terms of demand. And a way to think about it, because I think, I get asked this question sometimes, is if I had taken the GPUs that just came online in Q1 and Q2 in terms of GPUs and allocated them all to Azure, the KPI would have been over 40. And I think the most important thing to realize is that this is about investing in all the layers of the stack that benefit customers. And I think that’s hopefully helpful in terms of thinking about capital growth, it shows in every piece, it shows in revenue growth across the business and shows as OpEx growth as we invest in our people.

The cost that Microsoft is contending with here is not marginal cost, but rather opportunity cost: compute spent in one area cannot be used in another area; in the case of these earnings, Microsoft was admitting that they could have made their Azure number if they wanted to, but chose to prioritize their own workloads because, as CEO Satya Nadella noted later in the call, those have higher gross margin profiles and higher lifetime value.

It’s opportunity costs, not marginal costs, that are the challenge facing hyperscalers. How much compute should go to customers, and which ones? How much should be reserved for internal workloads? Microsoft needs to balance Azure — both for its enterprise customers and OpenAI — and its software business; Amazon needs to balance its e-commerce business, AWS, and its strategic investments in both Anthropic and OpenAI. Google has to balance GCP, its own strategic investment in Anthropic, and its consumer businesses.

Mythos

Last week Anthropic released announced Mythos, its most advanced model. And, in somewhat typical Anthropic fashion, it did so by focusing on its dangers; from the introductory post for Project Glasswing, the company’s initiative for leveraging Mythos to address security:

We formed Project Glasswing because of capabilities we’ve observed in a new frontier model trained by Anthropic that we believe could reshape cybersecurity. Claude Mythos Preview is a general-purpose, unreleased frontier model that reveals a stark fact: AI models have reached a level of coding capability where they can surpass all but the most skilled humans at finding and exploiting software vulnerabilities.

Mythos Preview has already found thousands of high-severity vulnerabilities, including some in every major operating system and web browser. Given the rate of AI progress, it will not be long before such capabilities proliferate, potentially beyond actors who are committed to deploying them safely. The fallout—for economies, public safety, and national security—could be severe. Project Glasswing is an urgent attempt to put these capabilities to work for defensive purposes.

In an Update last week I analogized Anthropic’s “disaster-porn-as-marketing-tool” approach to The Boy Who Cried Wolf; what’s important about that analogy is not just that the boy raised false alarms, but also that, in the end, the wolf did come. To that end, I wrote two weeks ago about the myriad of security issues that underpin all software, and my optimism that AI would solve these issues in the long run, even if it made things much worse in the short run. In other words, it’s actually not important whether or not Mythos represents a major security threat: if this model doesn’t, a future model will; to that end, I do support leveraging Mythos to proactively find and fix bugs before bad actors can find and exploit them.

At the same time, it’s also worth noting that there are other reasons for Anthropic to not make Mythos widely available, limiting access to a finite number of companies with a high capacity and willingness to pay. The first are those opportunity costs: Anthropic is already short on compute serving its current models; X was overrun with complaints and debates this weekend about Anthropic allegedly dumbing down Claude over the last month or so. Making Mythos more widely available — particularly to subscription plans that don’t pay per usage — would make the situation much worse.

In other words, Anthropic isn’t facing a marginal cost problem, but an opportunity cost problem: where to allocate its compute. Of course this could become a margin problem: I suspect that Anthropic is going to overcome its conservatism in terms of compute by acquiring more compute from hyperscalers and neoclouds, and paying dearly for the privilege.

The key to handling those costs will be to charge more for Claude going forward; that, by extension, means maintaining pricing power, which leads to a second benefit of not releasing Mythos broadly. Anthropic certainly faces competition from OpenAI; for both frontier labs, however, the real competition in the long run are open source models. Right now those primarily come from China, and a key ingredient in fast-following frontier models is distillation; from Anthropic’s blog:

We have identified industrial-scale campaigns by three AI laboratories—DeepSeek, Moonshot, and MiniMax—to illicitly extract Claude’s capabilities to improve their own models. These labs generated over 16 million exchanges with Claude through approximately 24,000 fraudulent accounts, in violation of our terms of service and regional access restrictions.

These labs used a technique called “distillation,” which involves training a less capable model on the outputs of a stronger one. Distillation is a widely used and legitimate training method. For example, frontier AI labs routinely distill their own models to create smaller, cheaper versions for their customers. But distillation can also be used for illicit purposes: competitors can use it to acquire powerful capabilities from other labs in a fraction of the time, and at a fraction of the cost, that it would take to develop them independently.

I absolutely believe this is a real problem, and wrote as much when DeepSeek R1 was released last year. I also think it’s in the interest of everyone other than the frontier labs to pretend that it isn’t; open source models are not subject to the frontier labs’ markup or compute constraints, which is exactly why it benefits most companies to have them available, whether or not they are distilled. Of course that doesn’t mean they are free to run: you still need to provide the compute.

Notice, however, how that makes stopping distillation even more of a priority for the frontier labs: first, they want to protect their margins. Second, however, their biggest cost is opportunity cost: the customers they can’t serve because they don’t have enough compute. To the extent they can make compute less useful for their potential customers — by stopping open source models from distilling their models — is the extent to which they can acquire that compute for themselves at more favorable rates.

Meta Muse

Mythos wasn’t the only new model announced last week: Meta released the first fruit of their new frontier lab as well. From the company’s blog post:

Today, we’re excited to introduce Muse Spark, the first in the Muse family of models developed by Meta Superintelligence Labs. Muse Spark is a natively multimodal reasoning model with support for tool-use, visual chain of thought, and multi-agent orchestration.

Muse Spark is the first step on our scaling ladder and the first product of a ground-up overhaul of our AI efforts. To support further scaling, we are making strategic investments across the entire stack — from research and model training to infrastructure, including the Hyperion data center…

Muse Spark offers competitive performance in multimodal perception, reasoning, health, and agentic tasks. We continue to invest in areas with current performance gaps, such as long-horizon agentic systems and coding workflows.

Muse Spark isn’t state of the art, but it’s in the game, and overall a positive first impression from Meta Superintelligence Labs. What is most notable to me, however, is the extent to which the last nine months of AI have made clear that CEO Mark Zuckerberg made the right call to embark on that “ground-up overhaul of [Meta’s] AI efforts”.

The trigger for O’Laughlin’s post that I opened this Article with was reasoning, where models using more tokens led to better answers; since then agents have exponentially increased token demand, as they can use LLMs continuously without a human in the loop. This is a huge driver in sky-rocketing demand for Claude, as well as OpenAI’s Codex. Moreover, this use case is so potentially profitable that not only is Anthropic’s revenue sky-rocketing, but OpenAI is pivoting its focus to enterprise.

Indeed, you can make the argument that one of OpenAI’s biggest challenges is the fact it has such a popular consumer product in ChatGPT. I, with my Aggregation Theory lens, have long maintained that that userbase was a big advantage for OpenAI, but that assumed that the company could effectively monetize it, which is why I have argued so vociferously for an advertising model. OpenAI has big projections for exactly that, but until that materializes, that big consumer base is a big opportunity cost in terms of OpenAI’s focus and compute. The company has, to its credit and in the face of widespread skepticism, made significant investments in more compute, but the temptation to allocate more and more compute to agentic use cases that enterprises will pay for, even at the expense of the consumer business, will be very large.

This puts Meta in a unique position relative to everyone else in the industry: unlike any of the hyperscalers or the frontier labs, Meta does not have an enterprise or cloud business to worry about. That means that serving the consumer market comes with no opportunity costs. Of course those opportunity costs would be much smaller anyways, given that Meta already has an at-scale advertising business to monetize usage. In other words, Meta may actually face less competition in winning the consumer space than it might have seemed a few months ago, simply because that is their primary focus — and because they have their own model, which means they don’t need to worry about not having access to the frontier labs (much of this analysis applies to Google, of course).

This, by the same token, is why Meta should open source Muse, just like they did Llama. The entities that will be the most hurt by widespread availability of a frontier model are other frontier labs, who will see their pricing power reduced and face increased competition for compute. This will make it even harder for them to bear the opportunity cost of pursuing the consumer market, leaving it for Meta.

Demand vs. Supply

So is “the era of Aggregation Theory…behind us”? On one hand, the insight that the way to create and maintain value will come from owning the customer is almost certainly going to continue to be the case. On the consumer side owning customers leads to advertising which provides the revenue to provide services to customers. On the enterprise side — which, I would note, has never been an arena where Aggregation Theory was meant to be applied — I think it’s likely that both Anthropic and OpenAI continue to move up the stack and deliver features that compete with software providers directly (an approach that is also in line with not making leading edge models publicly available).

On the other hand, O’Laughlin’s observation that we are and will continue to be compute constrained is an important one: companies will not be able to assume they can serve everyone, because serving one set of customers imposes the opportunity cost of not serving another. This won’t, at least in theory, last forever: at some point AI will be “good enough” for enough use cases that there will be enough compute capacity to take advantage of the fact that there really aren’t meaningful marginal costs entailed in serving AI; that theoretical future, however, feels further away than ever.

OpenAI is betting that this compute constraint — and the deals they have made to overcome it — will matter more than Anthropic’s current momentum with end users. From Bloomberg:

OpenAI told investors this week that its early push to dramatically increase computing resources gives it a key advantage over Anthropic PBC at a moment when its longtime rival is gaining ground and mulling a potential public offering.

The ChatGPT maker said it has outpaced Anthropic by “rapidly and consistently” adding computing capacity to support wider adoption of its software, according to a note the company sent to some of its investors after Anthropic announced a more powerful AI model called Mythos. The ambitious infrastructure build-out, criticized by some as too costly, has enabled OpenAI to better keep pace with rising demand for AI products, the memo states.

I’m less certain that this will be dispositive. When it comes to AI, distribution and transaction costs are still free — the two preconditions for Aggregators — which means that the winners should be those with the most compelling products. Those products will win the most users, providing the money necessary to source the compute to serve them; consider Anthropic’s deal to secure a meaningful portion of TPU supply, which, given the capacity constraints at TSMC, is ultimately an example of taking supply from Google. I suspect that Anthropic can take more, including already built hyperscaler and neocloud capacity. Yes, that compute will be more expensive, but if demand is high enough the necessary cash flow will be there.

In other words, my bet is that owning demand will ultimately trump owning supply, suggesting that the underlying principles of Aggregation Theory lives on. To put it another way, I think that OpenAI will need to win with better products, not just more compute; then again, if more compute is the key to better products, then does supply matter most? Regardless, they’ll certainly be focused on delivering both to the enterprise customers who are driving Anthropic’s astonishing growth. The real cost may be the consumer market they currently dominate, given that Meta has nothing to lose and everything to gain.

There is a weird phenomenon as a sports fan where the athletes on the field or court are older than you…and then they’re your age…and then they’re all younger than you; for me the last athlete I could look up to, at least in terms of age, was Tom Brady.

Tech companies are similar, in a way. I like to write about tech history, and the importance of origin stories for understanding company cultures, and I’m fortunate enough to have witnessed most of those origins. However, there are still some companies that pre-date me — the Tom Brady’s of the industry, if you will — and one of those is Apple, which turns 50 tomorrow.

Apple History

My first computer was a hand-me-down IBM-compatible 286 — I don’t even remember the brand — but I mostly cut my teeth building my own computers with overclocked Celeron chips in college, using parts procured by leveraging unsustainable dot-com era customer acquisition strategies (a unique email address meant a PayPal account with a free $25 and a single-use credit card with another free $25 used for a Value America account with a $50 off coupon). Needless to say I not only witnessed many of these companies’ births, but also their deaths!

There were Apple II’s at my elementary school, where I would type out programs in BASIC, but my first serious interaction with the company’s products was at the college newspaper doing layout in QuarkXPress; after I graduated I was smitten by the iMac G4 and its adjustable arm, and the GarageBand addition to the iLife suite; I ended up buying an iBook, and here I am, a quarter of a century later, typing this Article on a MacBook Pro.

In my history is much of Apple’s history. I missed the very early years, when the Apple I was a mere circuit board created by Steve Wozniak; Steve Jobs bought the parts for the initial batch on net-30 terms and paid them off by receiving cash-on-delivery from a computer shop in Mountain View; it was the Apple II, released in 1977, that made the company, and that was my first encounter with Apple. The Mac came out in 1984, and found its niche in desktop publishing; that’s how I came back to Apple in college. Apple, however, was struggling in the face of more capable modular Windows PCs, which I was happily building in the meantime.

It was OS X that changed Apple’s fortunes with nerds, and Jony Ive’s stunning designs that changed the value proposition for everyone else; iLife, meanwhile, made the Mac useful from day one. It was the combination of all three that made me a customer, and as the Internet destroyed lock-in, it was the fit and finish of the operating system and Apple’s independent developer ecosystem that made my two years at Microsoft with Windows a drag; then, in 2020, Apple’s differentiation came full circle: Macs were the fastest personal computers — particularly laptops — in the world.

There were, of course, other parts of the Apple story, including the iPod and, most importantly, the iPhone. Those were the products that made Apple the most valuable company in the world for years (today Apple is surpassed only by Nvidia). These products, however, might have been in a form that addressed a far larger market, but were still very much Apple, a company that, all these years later, faces no competition when it comes to integrating hardware and software.

Apple’s Competitors

What do I mean by “no competition”? Well, consider Apple’s nominal competitors through the years:

IBM: This is, perhaps, the most iconic photo from early Apple:

Jean Pigozzi via Andy Hertzfeld

The Apple I launched in a world where computing was primarily for the enterprise, and primarily happened on IBM’s mainframes. Increased accessibility of processors and memory, however, made hobbyist computers possible, which is exactly what the Apple I was.

In the late 1970s and very early 1980s, a new breed of personal computers were appearing on the scene, including the Commodore, MITS Altair, Apple II, and more. Some employees were bringing them into the workplace, which major corporations found unacceptable, so IT departments asked IBM for something similar. After all, “No one ever got fired…”

IBM spun up a separate team in Florida to put together something they could sell IT departments. Pressed for time, the Florida team put together a minicomputer using mostly off-the-shelf components; IBM’s RISC processors and the OS they had under development were technically superior, but Intel had a CISC processor for sale immediately, and a new company called Microsoft said their OS — DOS — could be ready in six months. For the sake of expediency, IBM decided to go with Intel and Microsoft.

IBM was, in the end, just a hardware maker; they couldn’t be bothered to make the software.

Microsoft: Software fell to Microsoft. Continuing from that 2013 Article:

The rest, as they say, is history. The demand from corporations for IBM PCs was overwhelming, and DOS — and applications written for it — became entrenched. By the time the Mac appeared in 1984, the die had long since been cast. Ultimately, it would take Microsoft a decade to approach the Mac’s ease-of-use, but Windows’ DOS underpinnings and associated application library meant the Microsoft position was secure regardless.

For decades after the fact, conventional wisdom was that Microsoft’s modular approach — the one that let me build my own computers — was unquestionably superior to Apple’s integration of hardware and software. In fact, it was Apple’s integration that kept the company afloat: all of those Macs used for desktop publishing were expensive, and gave Apple enough revenue to (barely) stay in business; the company’s brief foray into licensing Macintosh OS was a major contributor to the company nearly going bankrupt.

Or, to put it another way, Apple only briefly competed with Microsoft, and it nearly killed them.

Consumer Electronics Companies: It’s difficult to choose a company to represent the iPod era, because Apple didn’t really face any meaningful competition. There was Sony and the Discman, and Diamond and Creative with some of the first MP3 players, but the reality is that no one had the combination of hardware and software that made the iPod special; in this case, the software was iTunes, and putting iTunes on Windows is what propelled Apple far beyond the Macintosh, and laid the groundwork for what came next.

RIM, Palm, and Nokia: It was early smartphone makers who were, in the framing I am taking in this Article, the only true competition Apple has ever had. All three of these companies integrated hardware and software, which makes sense given that the smartphone category was so nascent — that’s when integration is particularly important.

The iPhone, however, was different in one important regard: RIM, Palm (which also sold phones with Microsoft’s Windows Mobile), and Nokia first and foremost made phones; the iPhone was a full-blown computer, built on a foundation of OS X. That, combined with the iPhone’s innovative multi-touch input method, resulted in a vastly more capable and compelling device that wiped out all three companies.

Android: Android is, in many respects, the Windows to Apple’s iOS — which was why many commentators predicted that Apple was doomed. One critical difference, however, is in the Article I excerpted above: whereas DOS came before the Mac, the iPhone came before Android. That meant that Apple had a critical mass of users and developers first, in contrast to the 1980s. Another difference is that the iPhone sold to end users, not IT departments, who actually cared about the look and feel of the device they were spending their money on. A third difference is that Apple had (and continues to have) the performance advantage, thanks to their investment in their own silicon, a stark difference from the dead end the company found itself in with the Mac.

Android is, of course, a big success, with more unit market share worldwide (although the iPhone has majority share in the U.S.). There is a place for modularity, and companies like Samsung have done well to build high-end Android-powered devices, with a host of Chinese companies in particular filling in the lower-end. And, it should be noted, that Google makes its own Pixel phones as well; that is true competition, albeit one that barely registers given Google’s commitment to the entire Android ecosystem (so few, if any Pixel-exclusive features, at least not for long), and Apple’s grip on the high-end of the market.

Perhaps Apple’s most interesting new product is one that takes the company full circle. The MacBook Neo is the cheapest Mac laptop ever, and has the company poised for major gains in the low-end of the market. Notably, in defiance of the assumption that modular offerings take share by being cheaper and “good enough”, Apple, by making everything from operating system to device to chip, is selling a computer that is both higher quality and has higher performance with lower component costs than the alternatives in its class; and, now that there is no more software lock-in — the Neo runs a browser and an AI chat client just like Windows machines do — Apple is poised to make major gains in its oldest market.

Apple Aggregates AI

More generally, Apple’s market share in all of its markets, including the phone, continues to increase over time, not decrease. This is happening despite the fact that Apple is not investing at a meaningful level — at least compared to its Big Tech peers — in AI server capacity, and has yet to ship the new AI-empowered Siri it promised nearly two years ago. The reason it doesn’t matter is that no matter how powerful AI becomes, you still need to access it with a device, and Apple, thanks to its integration of hardware and software, makes the best devices.

Now, according to Bloomberg, Apple is planning to leverage its position with end users to give access to multiple AI providers:

Apple Inc. plans to open Siri to outside artificial intelligence assistants, a major move aimed at bolstering the iPhone as an AI platform. The company is preparing to make the change as part of a Siri overhaul in its upcoming iOS 27 operating system update, according to people with knowledge of the matter. The assistant can already tap into ChatGPT through a partnership with OpenAI, but Apple will now allow competing services to do the same…

The company is developing new tools to allow AI chatbot apps installed via the App Store to integrate with the Siri assistant, said the people, who asked not to be identified because the plans haven’t been announced. The chatbots will also work with an upcoming Siri app and other features in the Apple Intelligence platform. That means, for instance, if users have Alphabet Inc.’s Google Gemini or Anthropic PBC’s Claude installed, they’d be able to send queries to those services from within the Siri voice assistant, just like they have been able to with ChatGPT since Apple Intelligence launched in 2024. The approach also should allow Apple to generate more money from third-party AI subscriptions through the App Store.

This isn’t quite Safari search, wherein Apple earns a revenue share from Google for searches made through the iPhone’s built-in browser, but given that AI assistants are largely monetized through subscriptions, it’s not far off: Apple will happily sell subscriptions through the App Store and take 30% of the price for the first year, and 15% after that. Owning the device means Apple gets to aggregate AI (and the company is already making $1 billion a year from chatbot subscriptions).

This is exactly what I expected after Apple announced that initial partnership with OpenAI; from a 2024 Update

Apple, probably more than any other company, deeply understands its position in the value chains in which it operates, and brings that position to bear to get other companies to serve its interests on its terms; we see it with developers, we see it with carriers, we see it with music labels, and now I think we see it with AI. Apple — assuming it delivers on what it showed with Apple Intelligence — is promising to deliver features only it can deliver, and in the process lock in its ability to compel partners to invest heavily in features it has no interest in developing but wants to make available to Apple’s users on Apple’s terms.

The company that owns the point of integration in the value chain never wants to have an exclusive supplier; it wants to commoditize its complements, which means creating a modular interface for multiple companies to compete on the integrator’s terms, which is exactly what these AI extensions for App Store apps sound like.

Of course there still is the matter of getting Apple Intelligence to work; this upcoming feature is separate from Apple’s deal with Gemini for foundation models for Siri. I explained the distinction in this Update, and concluded:

The big problem with this vision is that it assumed that Apple Intelligence would be competent, and it simply wasn’t; just as the iPhone search deal wouldn’t be worth much if the iPhone sucked, Siri chatbot integration isn’t worth much if Siri sucks. Now, however, Google is selling the underlying model to make Siri good, and their biggest hope is that they can pay Apple all of their money back — and more! — to have a money-making Gemini sit on top.

Apple will let the users decide who is on top; I’m sure the company would also be amenable to be paid to be the default!

Apple and OpenAI

Many people are taking a victory lap about Apple’s decision to not compete in AI models, claiming that the company is winning by not trying; I previously linked to Horace Dediu’s The most brilliant move in corporate history?, but it’s a good articulation of the argument:

The hyperscalers are now spending 94% of their operating cash flows on AI infrastructure. Amazon is projected to go negative free cash flow this year with as much as $28 billion in the red. Alphabet’s free cash flow is expected to collapse 90% from $73 billion to $8 billion. These companies used to be the greatest cash machines ever built. Now they’re borrowing money to keep the data center lights on…

And what are they getting for that $650 billion? AI services generate roughly $35 billion in total revenue or 5% of what’s being spent on infrastructure. There are dreams of more of course, but the business models of AI have yet to resonate, especially for consumers…

Apple didn’t miss the AI revolution. It just bet that the winners won’t be the ones who build the infrastructure. They’ll be the ones who own the customer and no one else on Earth owns the best customers.

Apple owns the best customers because it makes the best devices, thanks to its integration of hardware and software. And, as I recounted above, it is somehow, fifty years on, the only company of its kind. There is, however, an emerging threat that Apple is seeking to head off. Again from Bloomberg:

Apple Inc. awarded rare bonuses to iPhone hardware designers this week, aiming to stem a wave of departures to AI startups like OpenAI that are building their own devices. The company granted out-of-cycle bonuses worth several hundred thousand dollars to many members of its iPhone Product Design team, according to people with knowledge of the matter.

Apple’s leadership has grown increasingly concerned about the number of engineers being poached by potential rivals. OpenAI, which has tapped former Apple design chief Jony Ive to help design a new generation of AI-centric products, has emerged as a particular threat…OpenAI’s hardware division is run in part by Apple veteran Tang Tan. He used to oversee the iPhone product design team that’s receiving the bonuses. Tan’s group at OpenAI has hired several dozen Apple engineers, and not just ones who worked on the iPhone. The startup has lured employees who helped develop the iPad, Apple Watch and Vision Pro.

OpenAI isn’t just hiring designers; the company is also building out operations capabilities to be able to actually make the upcoming Ive-designed device at scale (presumably in China). Still, many are wondering about the status of OpenAI’s hardware device given the news about Sora; from the Wall Street Journal:

OpenAI is planning to pull the plug on its Sora video platform, a product it released to great fanfare last year that has since fallen from public view. The move is one of a number of steps OpenAI is taking to refocus on business and coding functions ahead of a potential initial public offering as soon as the fourth quarter of this year. CEO Sam Altman announced the changes to staff on Tuesday, writing that the company would wind down products that use its video models. In addition to the consumer app, OpenAI is also discontinuing a version of Sora for developers and won’t support video functionality inside ChatGPT, either.

OpenAI is in the middle of a strategy shift to redirect the company’s computing resources and top talent toward so-called productivity tools that can be used by both enterprises and individual users. Last week, OpenAI announced that it was combining its ChatGPT desktop app, coding tool Codex and browser into one “superapp.” The company expects the consolidated product to align its employees around a single vision.

In fact, cutting Sora but keeping the hardware initiative fits this strategy shift: Sora, along with the also indefinitely delayed adult-mode, were products that drive more attention, which lends itself to the more traditional consumer business model of advertising. Productivity, on the other hand, is a much better fit for enterprise, where Anthropic is making major gains. The problem, however, is that most consumers aren’t willing to pay for software; what they are willing to pay for are devices. This was the secret of the iPhone; from 2016’s Everything as a Service:

Apple has arguably perfected the manufacturing model: most of the company’s corporate employees are employed in California in the design and marketing of iconic devices that are created in Chinese factories built and run to Apple’s exacting standards (including a substantial number of employees on site), and then transported all over the world to consumers eager for best-in-class smartphones, tablets, computers, and smartwatches.

What makes this model so effective — and so profitable — is that Apple has differentiated its otherwise commoditizable hardware with software. Software is a completely new type of good in that it is both infinitely differentiable yet infinitely copyable; this means that any piece of software is both completely unique yet has unlimited supply, leading to a theoretical price of $0. However, by combining the differentiable qualities of software with hardware that requires real assets and commodities to manufacture, Apple is able to charge an incredible premium for its products.

OpenAI is approaching this space from the opposite direction: it has a massive consumer user base for ChatGPT, and an impressively large number of subscribers; it is also adding advertising. However, to truly monetize consumers the most attractive business model is the Apple model: integrated hardware and software.

Apple’s Real AI Threat

The truth is that Apple’s lack of investment in AI was always going to be a short to medium-term win: the company doesn’t have to spend on infrastructure, and everyone still needs a device. The real threat is in the long-term: what happens if AI becomes so good that it obviates traditional userinterfaces? Or, to put it another way, what if the point of integration that is most compelling is not a traditional operating system and hardware device, but rather AI and a dedicated device?

If this threat materializes, it won’t be with OpenAI’s initial offering; the smartphone is the ultimate form factor, and does so many jobs that depend on its flexibility and capability and 3rd-party ecosystem that no new entrant could hope to compete (indeed, Google and Android is arguably a bigger threat for this reason). However, just how capable might AI be not just next year, but in five years, or ten years? If ever a better interaction paradigm were to succeed the smartphone surely it will be rooted in AI — and Apple, by giving up now, won’t be in the game.

This absolutely is not a prediction. Indeed, if I had to bet, I would bet on Apple keeping its place:

First, there is the likelihood that the smartphone, thanks to its screen, connectivity, and battery life, is in fact the best device for AI, and that furthermore, AI will be just one capability alongside everything a smartphone already does.

Second, to the extent that AI inference moves to the edge, Apple has a big advantage thanks to its industry-leading chips.

Third, Apple always has the option of opening up its devices to allow for much deeper integration with 3rd-party AI providers other than OpenAI, in order to effectively fight off a potential threat.

It’s also worth noting that OpenAI has, in its relatively short life, managed to frame itself as a competitor to basically everyone in tech, from Google to Meta to Microsoft, only to find itself forced to pivot in the face of Anthropic and its focused approach on coding and productivity in the enterprise. The audacity of taking on everyone is impressive; the effectiveness of fighting everyone for everything may be less so.

Still, there is an angle here for OpenAI, and a point of vulnerability for Apple. The company made it fifty years with no one truly competing with its integrated business model; the fate of its next fifty years may rest on the question of just how compelling AI ends up being — and if OpenAI can out-Apple the original.

There is a weird paradox in terms of AI prognostication: on one hand, you don’t want to be the one to completely dismiss the most terrifying doomsday scenarios; who wants to be found out to be foolishly optimistic? At the same time, there is also pressure to give credence to the possibility that we are in a bubble, and all of this hype and spending is going to go belly up.

Sitting here in March 2026, however, on the morning of Nvidia’s GTC, I’ve come to a different conclusion: I don’t think we’re in a bubble (which, paradoxically, maybe is the truest evidence we are).

LLM Paradigms

Over the last couple of weeks, first in the context of Nvidia’s earnings, and then last week in the context of Oracle’s, I’ve talked about three LLM inflection points.

ChatGPT: The first LLM inflection point was the November 2022 launch of ChatGPT, which hardly needs an explanation. Yes, transformer-based large language models were introduced in 2017, and the capabilities were both impressive and growing, but under-appreciated; Stratechery started an interview series with Daniel Gross and Nat Friedman in October 2022 under the premise that there was an incredible new technology that was sorely lacking for product applications and startup energy.

Needless to say, that was entirely flipped on its head just weeks later. ChatGPT opened the eyes of the world to what LLMs were capable of, but the initial versions had two flaws that have stuck in many people’s minds, particularly those convinced that we are in a bubble.

The first flaw is that LLMs frequently got things wrong, and worse, would hallucinate when it didn’t know the answer. This made LLMs feel like something of a parlor trick: amazing when they work, but not something that you can count on. The second was related to the first: even in that flawed state LLMs were tremendously useful, but you needed to have an idea of what to use them for, and you needed to proactively take care to manage mistakes and verify the output in case it was hallucinated.

o1: The second LLM inflection point was the release of OpenAI’s o1 model in September 2024. By that point LLMs had improved tremendously, both thanks to new foundation models and also because of continued improvements in post-training; that meant that the stream of tokens that constituted an answer in ChatGPT or Claude was now much more likely to be right, and they were somewhat less likely to hallucinate. What made o1 different, however, was that it reasoned over its answer before delivering it to you. I explained in an Update at the time:

The big challenge for traditional LLMs is that they are path-dependent; while they can consider the puzzle as a whole, as soon as they commit to a particular guess they are locked in, and doomed to failure. This is a fundamental weakness of what are known as “auto-regressive large language models”, which to date, is all of them.

Reasoning models self-evaluate: they work through an answer and then consider if the answer is correct, or if they should consider other alternatives. To put it in terms of the weaknesses I identified above, they were internally proactive in terms of managing mistakes, reducing the burden on the user to continually actively guide the LLM, and the results were remarkable. From my perspective, if the brilliance of ChatGPT was in making LLMs much more readable and useful, the brilliance of o1 was in making LLMs much more reliable and essential.

Opus 4.5: Anthropic released Opus 4.5 on November 24, 2025, to relatively little fanfare; then, at some point in December, Claude Code with Opus 4.5 suddenly seemed to be able to do things that were never possible previously. OpenAI released GPT-5.2-Codex around the same time, on December 18, and it was similarly capable. People had been talking about “agents” for a while; suddenly, however, both Claude and Codex were actually accomplishing tasks — some of which took hours — and doing them correctly.

That bit about the Opus 4.5 model’s release date is interesting, however: the key thing about agentic workloads is that they are about more than the model, or using the model recursively, like o1. Rather, a critical component of making agentic workloads work is the “harness”, i.e. the software that actually controls the model.

To put it another way, Claude Code and OpenAI’s Codex actually abstract the user away from the model: you give instructions to an agent, which actually directs the model; critically, the agent can also use other deterministic tools as well, which means that it can verify its results. To put it in the context of coding, in paradigm one an LLM would generate code; in paradigm two an LLM would think about the code it was generating and iterate towards a better answer; in this paradigm an agent directs a model to generate code, then checks to see if the code actually works, and if it doesn’t tries again, all without the user needing to be involved.

In other words, many of the biggest flaws from the original ChatGPT have been substantially mitigated, at least for verifiable use cases like coding: LLMs are much more likely to be right the first time, they reason over their results to increase their chances, and now agents actively verify the results without humans needing to be in the loop. That leaves one flaw: actually figuring out what to use these for.

The Decreased Need for Agency

The reason I’ve been writing about these three inflection points over the last couple of weeks has been to explain why it is that the industry is so compute constrained and why the massive investment in capex by the hyperscalers is justified.

The first paradigm required a lot of compute for training, but inference — actually answering a question — was relatively efficient: you simply sent the user whatever the model spit out.

The second paradigm dramatically increased the amount of computing needed for inference, for two reasons: first, generating an answer required a lot more tokens, because all of the “reasoning” required tokens, in addition to the answer itself. Second, the fact that reasoning made the models so much more useful meant that they were used more, which drove increased token usage in its own right.

It’s the third paradigm, however, that has truly tipped the scales in favor of capex expenditure not being speculative investment but rather badly needed investment in meeting demand that far exceeds supply. First, generating an answer will often entail multiple calls to a reasoning model. Second, the agent itself needs compute, and that compute — and the tools the agent uses — is better done by CPUs than GPUs. Third, agents are another step function increase in usefulness, which means they are going to be used even more than even reasoning models in a chatbot.

It’s how this third point will be manifested that I think is under-appreciated. After all, far more people use chatbots than use agents, and I would make the case that most people are not using chatbots as much as they should! It’s been a question of agency: to get the most from AI requires actually taking the initiative to use AI; I wrote in 2024’s MKBHD’s For Everything:

Large language models are intelligent, but they do not have goals or values or drive. They are tools to be used by, well, anyone who is willing and able to take the initiative to use them. I don’t think either Brownlee or I particularly need AI, or, to put it another way, are overly threatened by it…The connection between us and AI, though, is precisely the fact that we haven’t needed it: the nature of media is such that we could already create text and video on our own, and take advantage of the Internet to — at least in the case of Brownlee — deliver finishing blows to $230 million startups.

How many industries, though, are not media, in that they still need a team to implement the vision of one person? How many apps or services are there that haven’t been built, not because one person can’t imagine them or create them in their mind, but because they haven’t had the resources or team or coordination capabilities to actually ship them?

This gets at the vector through which AI impacts the world above and beyond cost savings in customer support, or whatever other obvious low-hanging fruit there may be: as the ability of large language models to understand and execute complex commands — with deterministic computing as needed — increases, so too does the potential power of the sovereign individual telling AI what to do. The Internet removed the necessity — and inherent defensibility — of complex cost structures for media; AI has the potential to do the same for a far greater host of industries.

It’s interesting to read that two years on, realize that I was writing about the latest paradigm shift well before it happened, and yet feel completely blown away by that paradigm shift all the same. That’s how big of a deal actually functional agents are: you can see them coming and yet still be amazed when they arrive — and, as one must say with everything related to AI, in a form that is the worst they will ever be.

It’s the implications on agency, however, that are the most profound: yes, you need agency to use agents, and yes, the number of people who will have that agency are probably far fewer than those who might use a chatbot. Of course you can make the (almost certainly accurate) case that chatbots will become agent managers in their own right, but the more critical observation is that by abstracting humans away from direct model management any one single human can control multiple agents.

What this means in terms of compute — and by extension, economic impact — is that it actually won’t require that many people with agency to drastically increase the amount of compute that is actively utilized to create products with meaningful economic impact. In other words, the rise of agents doesn’t just mean a dramatic increase in compute, but also a narrowing of the need for widescale adoption by humans for that demand to manifest. Yes, AI still needs agency; it just doesn’t need agency from that many people for its impact to be profound.

Enterprise Economic Imperatives

Apple-focused media, in the wake of the recent MacBook Neo launch, latched onto comments from Asus CFO Nick Wu on the company’s recent earnings call describing the $599 computer as “a shock to the entire market”; equally interesting, however, was how Wu sought to downplay the Neo’s potential effects on that market:

Actually, we heard about the MacBook Neo shipments coming online back in the second half of last year. So we made some internal preparations. But after the product officially released, we found the specs to have some limitations. For example, the memory is not upgradable, and it only has 8 gigabytes of memory. So this may limit certain applications. So I think when Apple positioned the product, it’s probably focused more on content consumption. This differs somewhat from mainstream notebook usage scenarios because in that case, the Neo feels more like a tablet because tablets are mostly for content consumption.

This feels like a bit of a cop-out, given just how capable the Neo’s processor is, and how well Mac OS operates on 8GB of RAM, thanks in part to Apple’s deep integration of hardware and software; at the same time, Wu is tapping into something that is true, which is that most consumers mostly do just want to consume content (which, I would add, means he should be more worried about the Neo, not less). This is why your favorite productivity application always ends up pivoting to the enterprise: it is companies who are willing to pay for productivity, because they are the ones actually paying for the workers who they want to be more productive.

It’s reasonable to expect this to apply to AI as well: the most compelling consumer applications of AI, at least in the near term, are Google and Meta’s advertising businesses, which sit alongside content. By the same token, it was always unrealistic for OpenAI to think that it could convert more than a small percentage of consumers into subscribers; that’s both why an ad model is essential, and also why that won’t be enough to pay the bills. It’s definitely the case that most people don’t want to pay for AI; it remains to be seen if they want to use it enough to make the ad model work.

That is another way of saying that Anthropic got it right by focusing almost entirely on the enterprise market: companies have a demonstrated willingness to pay for software that makes their employees more productive, and AI certainly fits the bill in that regard. What makes enterprise executives truly salivate, however, is the prospect of AI not simply eliminating jobs, but doing so precisely because that makes the company as a whole more productive.

It’s always been the case, even in large companies, that a relatively small number of people actually move the needle and drive the company forward in meaningful ways. That drive, however, has been filtered through a huge apparatus, filled with humans, who accelerate the effort in some vectors, and retard it in others. That apparatus makes broad impact possible, but it carries massive coordination costs.

Agents, however, will tilt much more heavily towards pure acceleration, making those drivers of value much more impactful. I’m sympathetic to the argument that the best companies will want to use AI to do more, not simply save money; the reality of large organizations, however, is that the positive impact of AI will not be in eliminating jobs, but rather replacing hard-to-manage-and-motivate human cogs in the organizational machine with agents that not only do what they are told but do so tirelessly and continuously until the job is done.

This only makes the argument that we are not in a bubble that much more compelling:

First, all of the weaknesses of LLMs are being addressed by exponential increases in compute.

Second, the number of people who need to wield AI effectively for demand to skyrocket is decreasing.

Third, the economic returns from using agents aren’t just impactful on the bottom line, but the top line as well.

In this context, is it any wonder that every single hyperscaler says that demand for compute exceeds supply, and that every single hyperscaler is, in the face of stock market skepticism, announcing capex plans that blow away expectations?

This is also why the impending wave of layoffs that are going to be credited to AI shouldn’t be completely dismissed as a useful cover for correcting over-hiring decisions in the COVID era, or right-sizing compensation structures in the wake of multiple contractions. That is all true!

At the same time, it’s worth considering that companies become bloated because that has long been the only way to scale, and it’s hard to know at what point the diminishing returns that come from the drag of coordination costs and a sprawling workforce outweigh the benefits of the marginal employee; you only find that point when you have blown past it, and it’s hard to go backwards.

AI, however, not only gives the aforementioned excuse to undo that bloat, but also moves the “rightsize” point significantly towards a much smaller workforce. More and more companies are not simply going to wonder if they hired too much for a pre-AI world, but also if they hired too much for a post-AI world; the most forward-looking and future-proof approach will likely be to cut more rather than less, with the hope that those who remain have no choice but to rebuild scale with agents. After all, if they don’t, dramatically smaller competitors built with AI from the beginning will soon be nipping at their heels with both smaller cost structures and more capabilities that will structurally increase over time.

There is a good chance this is going to get ugly; I’m not advocating for this outcome, rather analyzing why it is probably going to happen. The economic imperatives are going to be impossible to resist, and will fuel demand for even more compute over time, further supporting the case that this is no bubble.

Agents and the AI Value Chain

Another important bubble question is about the sky-high valuations of Anthropic and OpenAI: sure, maybe all of this stuff is real, but if models are a commodity, is there any profit to be made? Horace Dediu raises these questions at Asymco and wonders if Apple is executing The Most Brilliant Move in Corporate History:

Here is where Apple’s bet becomes genius. AI models are commoditizing faster than anyone predicted. Software and hardware both have tendencies to commodify. Protections exist but they have to do with integration and distribution. DeepSeek built a model for $6 million that matches systems costing $100 million. Open source models now power 80% of startups seeking VC funding. The moat these companies are spending hundreds of billions to build is evaporating.

Apple understood this before anyone else. It didn’t build its own AI model, it licensed Google’s Gemini for about $1 billion a year. Why spend $100 billion building a factory when outsourcing costs a billion? And if a better model appears next year, Apple just switches vendors…Apple didn’t miss the AI revolution. It just bet that the winners won’t be the ones who build the infrastructure. They’ll be the ones who own the customer and no one else on Earth owns the best customers.

I think that nearly all of these assertions were defensible during the first LLM paradigm. It didn’t take long for multiple base models to be more than good enough for what most people use LLMs for, like, say, cooking or basic medical advice, or as a therapist or companion. Moreover, it was reasonable to expect that models of this quality would soon be able to run locally; I made the case that this was Apple’s opportunity myself back when their own models — which they absolutely did try to build, contra Dediu — failed to ship.

The reasoning paradigm, however, blew a significant hole in the local inference case. Not only do reasoning models require fast compute, given the number of tokens generated, but they also need exponentially more memory to accommodate much larger context windows, which is the biggest limitation of local models. Apple makes incredible chips with a compelling unified memory architecture that makes basic inference more plausible for their devices than anyone else; there is also no scenario where capable reasoning models that are remotely competitive with cloud-based models are running locally in the foreseeable future.

It is agents, however, that may strike the fatal blow to Dediu’s argument. Specifically, I noted above that what made Opus 4.5 compelling was not the model release itself, but changes to the Claude Code harness that made it suddenly dramatically more useful. What this means is that model performance isn’t the only thing that matters: the integration between model and harness is where true agent differentiation is found.

This is a very big deal when it comes to figuring out the future structure of the AI industry and where profits will flow, because profits flow away from modular parts of the value chain — which are commoditized — and flow towards integrated parts of the value chain, which are differentiated. Apple is of course the ultimate example of this: its hardware is not commoditized because it is integrated with their software, which is why Apple can charge sustainably higher prices and capture nearly the entirety of the PC and smartphone sector profits.

It follows, then, that if agents require integration between model and harness, that the companies building that integration — specifically Anthropic and OpenAI (Gemini is a strong model, but Google hasn’t yet shipped a compelling harness) — are actually poised to be significantly more profitable than it might have seemed as recently as late last year. And, by the same token, companies who were betting on model commoditization may struggle to deliver competitive products.

Fast forward to last week, however, when Microsoft revealed how they will handle the potential business impact of AI reducing seats, which is a bit of a problem for their seat-based business model: the company is going to bundle AI into a new higher-tiered enterprise offering, E7, which is going to cost twice as much — $99 per seat per month — as the formerly top-of-the-line E5. That’s a big increase, which Microsoft needs to justify with AI that actually makes those seats more productive, and the product they launched with the new bundle was Copilot Cowork.

If the “Cowork” name sounds familiar, it’s because this is basically the enterprise version of Claude Cowork, a GUI-ified version of Claude Code that the company released earlier this year. There are important differences with the Microsoft version, including the fact that the latter runs in the cloud and is grounded in your organizational data, with all of the permission and access policies that go with it. What is crucial, however, is that Copilot Cowork — unlike the Copilot chatbot — is not model agnostic: Cowork is an agent, which means it needs both a model and a harness, and those are two integrated pieces, not modular components.

The implications of this are significant: Microsoft is admitting, at least for now, that delivering a truly compelling agentic product that enterprises are willing to pay for means abandoning their stated goal of being model agnostic; that, by extension, raises the possibility that models are not and will not be commodities, because agents require more than models.

This certainly raises questions about Apple’s decision to merely license Gemini and build a harness themselves in the form of new Siri. Microsoft decided that they couldn’t deliver a compelling product by going that route; what has Apple done to inspire faith that they can do a better job? If anything, the company’s saving grace is the point that Dediu ended with: consumers may simply not care that much about agents, in which case Apple will be fine with good enough, even as Microsoft, with enterprise customers who do care, realizes it needs to share more margin than it might want to with Anthropic.

What matters in terms of this Article, however, is that if agents are making Anthropic and OpenAI the points of integration in the value chain, then the bubble argument that these companies are overvalued, or that the massive investments other companies are making on their behalf in data centers is unwarranted, may not be correct.

I must, in the end, address my opening parenthetical: I’ve long maintained that there is no need to be worried about a bubble as long as everyone is worried about a bubble; it’s the moment when caution is flung to the wind and assurances are made that this is definitely not a bubble that we might actually be in one. And, well, I think the rise of agents means we are not in a bubble. The capex is warranted, and Anthropic and OpenAI look more durable than ever. If my declaring there is no bubble means there is one, then so be it!

Just because you do not take an interest in politics doesn’t mean politics won’t take an interest in you. ― Pericles

This is not an Article about the campaign being waged by the U.S. against Iran, but it’s a useful — and timely — analogy. There is a never-ending debate that can be had about the concept of International Law and who might be violating it. Some will argue that the U.S. is in violation for the attacks; others will note that Iran has been serially violating International Law with both its overt actions and its support of terror networks for my entire life.

What is important to note is that the entire debate is ultimately pointless: the very concept of “international law” is fake, not because pertinent statutes and agreements don’t exist, but because their effectiveness is ultimately rooted in their enforceability. That, by extension, means there must be an entity to enact such enforcement, with the capability to match, and such an entity does not exist.

Yes, there is the United Nations, but said body only operates by the agreement of its members, and their willingness to subjugate themselves to not only its edicts, but to also put forward the capabilities to enforce its mandates. In other words, the only agents that matter are nation states themselves, and the relative power of those nation states is not a function of lawyers and judges but rather their ability to project force and coerce others.

To put it another way, if, after this weekend, you want to hold onto the concept of International Law, then realize the debate has been resolved: Iran was in violation, because their military just had its clock cleaned by the U.S., which means the U.S. decides who is right and who is wrong.

Anthropic vs. The Department of War

While most of the U.S., and certainly the rest of the world, was preoccupied with the happenings in Iran, another fervent debate has been ongoing in tech. Once again one of the parties is the United States itself, but the other entity in question is a private company, Anthropic. From the Wall Street Journal:

The federal government will stop working with Anthropic and designate the artificial intelligence company a supply-chain risk, a dramatic escalation of the government’s clash with the company over how its technology can be used by the Pentagon. While Anthropic’s relationship with the administration hit a new low, rival OpenAI said late Friday that it reached an agreement with the Defense Department to have its models used in classified settings, until recently a status only held by Anthropic. Friday’s quick-fire developments between the Pentagon and two Silicon Valley darlings are poised to shape the future of how the federal government and, particularly the Pentagon, uses cutting-edge AI tools.

In a narrow set of cases, we believe AI can undermine, rather than defend, democratic values. Some uses are also simply outside the bounds of what today’s technology can safely and reliably do. Two such use cases have never been included in our contracts with the Department of War, and we believe they should not be included now:

Mass domestic surveillance. We support the use of AI for lawful foreign intelligence and counterintelligence missions. But using these systems for mass domestic surveillance is incompatible with democratic values. AI-driven mass surveillance presents serious, novel risks to our fundamental liberties. To the extent that such surveillance is currently legal, this is only because the law has not yet caught up with the rapidly growing capabilities of AI. For example, under current law, the government can purchase detailed records of Americans’ movements, web browsing, and associations from public sources without obtaining a warrant, a practice the Intelligence Community has acknowledged raises privacy concerns and that has generated bipartisan opposition in Congress. Powerful AI makes it possible to assemble this scattered, individually innocuous data into a comprehensive picture of any person’s life—automatically and at massive scale.

Fully autonomous weapons. Partially autonomous weapons, like those used today in Ukraine, are vital to the defense of democracy. Even fully autonomous weapons (those that take humans out of the loop entirely and automate selecting and engaging targets) may prove critical for our national defense. But today, frontier AI systems are simply not reliable enough to power fully autonomous weapons. We will not knowingly provide a product that puts America’s warfighters and civilians at risk. We have offered to work directly with the Department of War on R&D to improve the reliability of these systems, but they have not accepted this offer. In addition, without proper oversight, fully autonomous weapons cannot be relied upon to exercise the critical judgment that our highly trained, professional troops exhibit every day. They need to be deployed with proper guardrails, which don’t exist today.

To our knowledge, these two exceptions have not been a barrier to accelerating the adoption and use of our models within our armed forces to date.

The Department of War has stated they will only contract with AI companies who accede to “any lawful use” and remove safeguards in the cases mentioned above. They have threatened to remove us from their systems if we maintain these safeguards; they have also threatened to designate us a “supply chain risk” — a label reserved for US adversaries, never before applied to an American company — and to invoke the Defense Production Act to force the safeguards’ removal. These latter two threats are inherently contradictory: one labels us a security risk; the other labels Claude as essential to national security.

Regardless, these threats do not change our position: we cannot in good conscience accede to their request.

I actually didn’t realize before this episode that the National Security Agency (NSA) is a part of the Department of War; that certainly provides useful context around the surveillance point. And, as we saw a decade ago with the Snowden revelations, the NSA can be both aggressive and creative in its interpretations of what is legal in terms of surveillance. One might have hoped that telecom companies in particular might have taken a stand like Anthropic did.

At the same time, what is the standard by which it should be decided what is allowed and not allowed if not laws, which are passed by an elected Congress? Anthropic’s position is that Amodei — who I am using as a stand-in for Anthropic’s management and its board — ought to decide what its models are used for, despite the fact that Amodei is not elected and not accountable to the public.

And, on the second point, who decides when and in what way American military capabilities are used? That is the responsibility of the Department of War, which ultimately answers to the President, who also is elected. Once again, however, Anthropic’s position is that an unaccountable Amodei can unilaterally restrict what its models are used for.

It’s worth noting that there are reports that Anthropic’s concerns may be broader than just fully autonomous weapons; from Semafor:

Anthropic is one of the few “frontier” large language models available for classified use by the US government because it is available through Amazon’s Top Secret Cloud and through Palantir’s Artificial Intelligence Platform, which is how its Claude chatbot ended up appearing on the screens of officials who were monitoring the seizure of then-Venezuelan President Nicolás Maduro…

Soon after the Maduro raid, during a regular check-in that Palantir holds with Anthropic, an Anthropic official discussed the operation with a Palantir senior executive, who gathered from the exchange that the AI startup disapproved of its technology being used for that purpose. The Palantir executive was alarmed by the implication of Anthropic’s inquiry that the company might resist the use of its technology in a US military operation, and reported the conversation back to the Pentagon, a senior Defense Department official said.

Anthropic denied it objected to whatever involvement Claude may have had in the Maduro raid, but the Semafor story resonates given the trend in some tech circles to resist any involvement in military operations. And, to that end, one could argue that this stand-off is ending as it should: Anthropic and its models will be removed from the Department of War tech stack, and an alternative will take their place.

North Korea and Nuclear Weapons

Amodei has been outspoken about other aspects of AI and national security; from Bloomberg in January:

Anthropic Chief Executive Officer Dario Amodei said selling advanced artificial intelligence chips to China is a blunder with “incredible national security implications” as the US moves to allow Nvidia Corp. to sell its H200 processors to Beijing. “It would be a big mistake to ship these chips,” Amodei said in an interview with Bloomberg Editor-in-Chief John Micklethwait at the World Economic Forum in Davos, Switzerland. “I think this is crazy. It’s a bit like selling nuclear weapons to North Korea.”

This rather raises the stakes of a messy procurement decision: consider the implications if we take Amodei’s analogy literally.

Start with Iran: beyond the fact that Iran has been responsible for the deaths of thousands of Americans throughout the Middle East and beyond, one of the arguments for the U.S. intervention is that Iran continues to pursue nuclear weapons capabilities. It’s North Korea that shows why: North Korea doesn’t need to buy nuclear weapons, because they already have them, and it certainly makes any sort of potential military action against them considerably more complicated. Nuclear weapons make you an effective lawyer in the (nonexistent1) court of international law!

In short, nuclear weapons meaningfully tilt the balance of power; the extent that AI is of equivalent importance is the extent to which the United States has far more interest in not only what Anthropic lets it do with its models, but also what Anthropic is allowed to do period.

In conjunction with the President’s directive for the Federal Government to cease all use of Anthropic’s technology, I am directing the Department of War to designate Anthropic a Supply-Chain Risk to National Security. Effective immediately, no contractor, supplier, or partner that does business with the United States military may conduct any commercial activity with Anthropic.

This would decimate Anthropic: at a bare minimum the company relies on cloud hosting from AWS, Microsoft, and Google, all of which have contracts with the Department of War; I imagine the same applies to Nvidia. Fortunately for the company, Hegseth’s declaration does seem out of step with the law, which limits Hegseth’s authority to work covered by U.S. government contracts; in other words, AWS could still serve Anthropic models, as long as it doesn’t use Anthropic models for any of its services offered to the U.S. government.

Regardless, this is an extreme measure that has been met with near universal dismay, even amongst people who are sympathetic to the idea that a private company should not have veto power over the U.S. military. Why would the U.S. government want to kneecap one of its AI champions?

In fact, Amodei already answered the question: if nuclear weapons were developed by a private company, and that private company sought to dictate terms to the U.S. military, the U.S. would absolutely be incentivized to destroy that company. The reason goes back to the question of international law, North Korea, and the rest:

International law is ultimately a function of power; might makes right.

There are some categories of capabilities — like nuclear weapons — that are sufficiently powerful to fundamentally affect the U.S.’s freedom of action; we can bomb Iran, but we can’t North Korea.